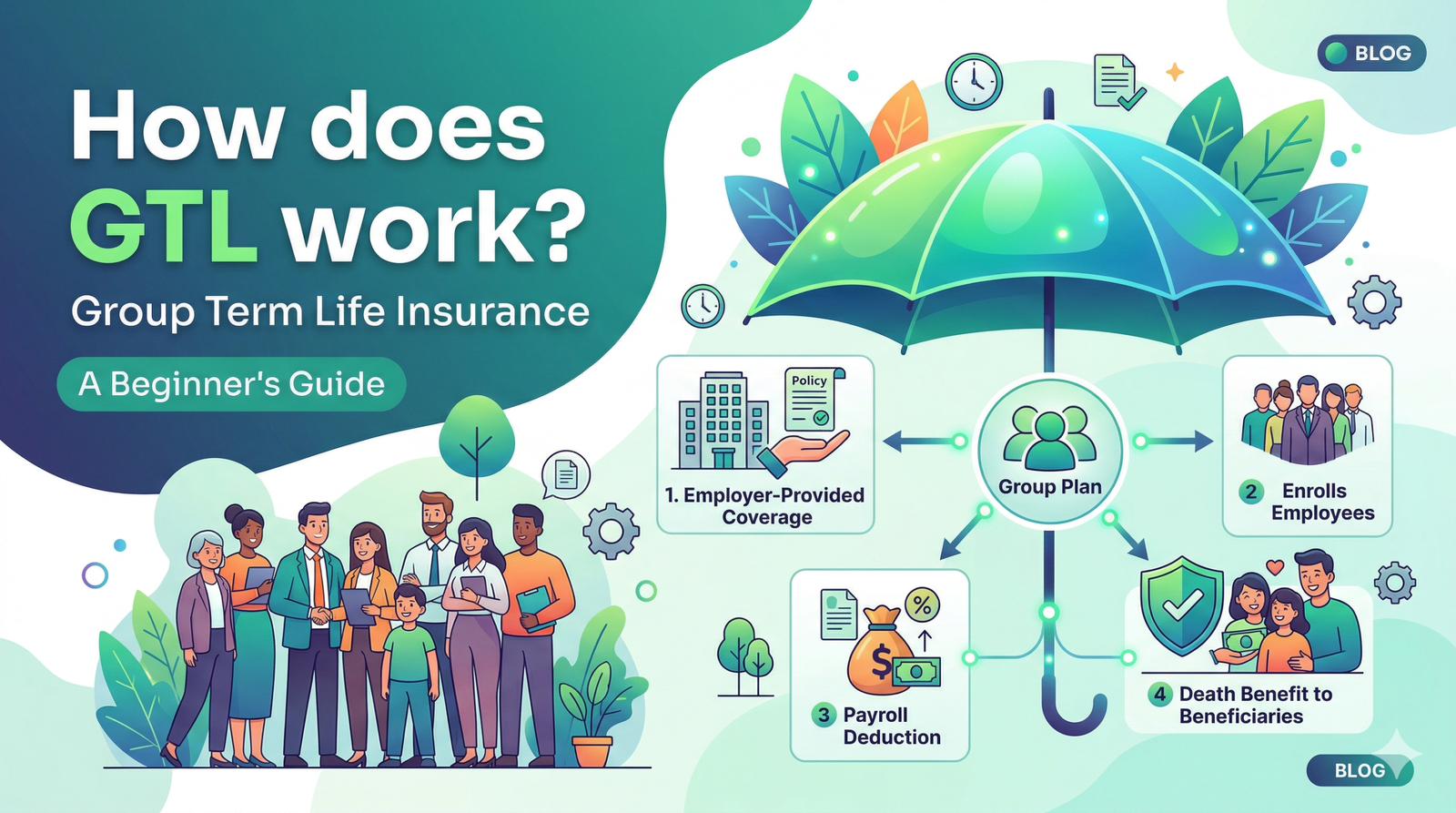

GTL on paycheck stands for Group Term Life Insurance. It is an employer-provided benefit that might show up as a part of your deductions. Learning about GTL and common employer-provided benefits that offer life insurance coverage to employees is of utmost importance. Need a paystub fast? Create one instantly with our simple and reliable paystub generator.

This blog explores all about group term life insurance and when it becomes taxable. Let’s take a deep dive into this.

What is GTL on paycheck?

GTL on paystub stands for Group Term Life Insurance. It’s an employer-provided life insurance benefit. It happens when your policy exceeds $50,000, and you’ll see the excess amount as taxable income. This is in accordance with the IRS section 79 & IRS Publication 15-B.

The GTL on paycheck shows the taxable life insurance benefits from your employer. This amount is not deducted from your paycheck, but it is the imputed income that adds to your taxable wages.

The GTL acronym might appear as GTLI or LIFE IMP, which depends on your employer’s tool. GTL on paystub reflects what the IRS considers taxable fringe benefits.

How does GTL work?

Group Term Life on Paycheck protects your loved ones by paying them a death benefit if you die while the coverage is still active. Many employers offer group term life insurance coverage as a benefit for their employees.

The employer-sponsored group term life insurance is offered to all employees of the company as it is more affordable than buying term life insurance as an individual, though it might have lower coverage amounts as well.

If you elect a group term life insurance, you will see it listed on your paystub or other benefits and deductions from your employer, along with the amount you pay each month in premiums. The description is shortened as GTL, but it might be written out in full or some other way, like life deduction.

The employer and the benefits provider it chooses shall dictate the terms of life insurance coverage. The group policies offer either a flat-rate benefit amount or one that is a multiple of salary, even though with a maximum coverage gap, and this coverage ranges from $50,000 to $500,000.

How can you calculate GTL imputed income?

In order to calculate your GTL imputed income, follow these steps:

Formula: Coverage amount – $50,000 / 1,000 * IRS Monthly Rate * 12 months

Example :

A 45-year-old with $150,000 coverage, which has a $100,000 excess.

At $0.15 per $1,000 monthly.

$0.15 * 100 * 12 = $180 annual imputed income.

What is GTL on paystub when it becomes taxable?

The GTL becomes taxable when coverage exceeds $50,000. The cost above this threshold is imputed income and is subject to FICA taxes. Coverage for spouse and dependents over $2,000 is also taxable. These rules come from IRS Section 79.

The federal income tax does not apply to this benefit. It is a non-cashable benefit that is subject to only FICA taxes. The $50,000 threshold is a minimum level set by the IRS.

If your employer’s life insurance policy is worth $100,000, then the first $50,000 is tax-free. The remaining $50,000 is treated as GTL imputed income, which is based on your age and the IRS premium table.

How is GTL reported on the W-2 Form?

Your W-2 shows GTL in boxes 1, 3, and 5, part of your taxable wages. It’s also listed alone in box 12, Code C. So, what exactly is GTL? That stands for group Term Life insurance. The number there isn’t the full benefit; it’s just the taxable piece. Why does this matter so much?

Box 12 Code C tracks how much of your life insurance plan gets taxed. You won’t find a clear label elsewhere. This value comes straight from payroll data at year-end. Did you know it matches your actual paystub entry?

The GTL amount on your December paystub should line up with what’s on your W-2. Any gap could mean an error in reporting. Review both carefully before tax day arrives.

If you’re unsure about how taxes apply to group life coverage, check our guide on reading a W-2. The breakdown covers every box, including Code C.

Advantages of GTL

The following are the advantages of GTL:

- Group Term Life Insurance is affordable, with rates as low as five cents per $1,000 coverage.

- GTL is a guaranteed issue, which means each and every one who applies for it is approved.

- Group Term Life Insurance complements other employer-sponsored benefits like disability insurance to maximize your financial protection.

Disadvantages of GTL

The following are the disadvantages of GTL:

- GTL tends to have lower coverage amounts, so it might not provide the right amount of financial protection you need.

- Group term policies reduce the benefit as you age, introducing confusion as you try to figure out how much coverage you have.

- Some group term insurance policies will increase your premium as you age, in five-year age groupings.

Key Takeaways

Employer-sponsored group term life insurance provides affordable coverage for employees and their families. Its lower costs, guaranteed qualification, and automatic payroll deductions—easily tracked using a paystub generator free tool complement other employee benefits, such as health insurance, to provide solid financial protection for your loved ones. However, GTL has drawbacks, including limited coverage amounts and a lack of portability if you leave the company.

FAQs

1) What does GTL stand for?

GTL stands for group term life insurance.

2) What is GTL meaning?

GTL means that they are enrolled in an employer-sponsored plan that exceeds $50,000 worth of coverage.

3) What does GTL mean for benefits?

GTL insurance plans are a popular benefit provided by a majority of employers to their full-time employees.

4) What is GTL’s claim process like?

GTL simplifies the application process with tools like text-to-sign and electronic submission, making sure convenience for agents and clients alike.

5) What is the waiting period in GTL?

GTL waiting period is from 6 to 12 months.

6) How to get a refund from GTL?

You should contact the Advanced Pay Service Department and press 0 to speak with a GTL representative to request a refund.

7) Why am I getting paid for group term life?

You’re getting paid for group term life because you have enrolled in an employer-sponsored, group term life insurance plan, which exceeds the $50,000 worth of coverage.

8) Can you cash out group term life insurance?

No, it is not possible to cash out group term life insurance.

9) What is GTL top up in salary slip?

A GTL top up in salary slip, which showcases a deduction for additional life insurance coverage beyond the company-paid policy.

10) How do I check my GTL balance?

To check the GTL balance, create a teleport account, make the deposits, and view the balance through the ConnectNetwork website.